Why Gas Prices Rise Faster Than They Fall

Control what matters in wealth planning with Financial Gravity guidance that aligns taxes, risk, costs, and legacy for lasting confidence.

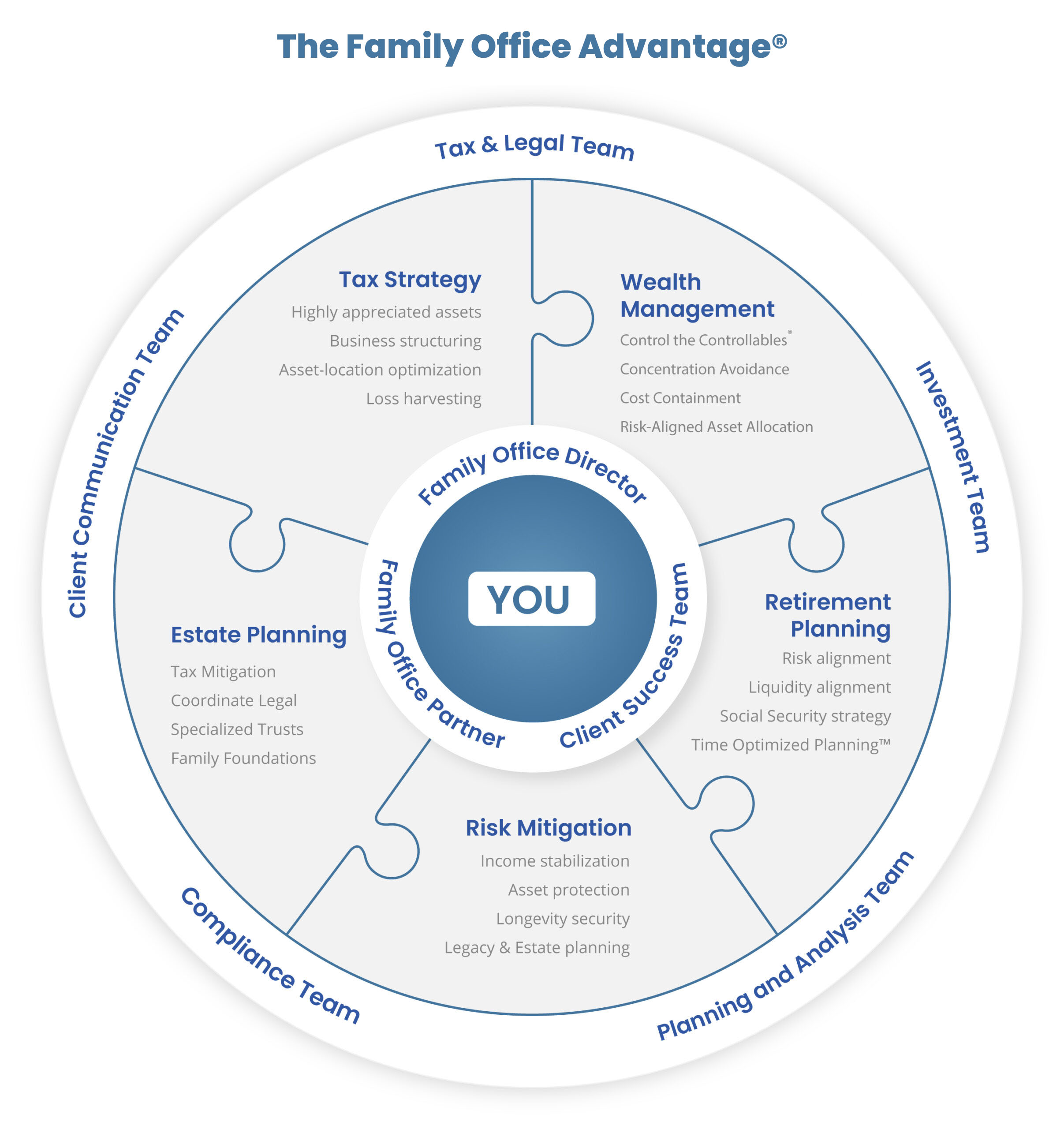

Control the Controllables

Control what matters in wealth planning with Financial Gravity guidance that aligns taxes, risk, costs, and legacy for lasting confidence.

Why Tax Season Feels So Stressful

Bring clarity to tax season with coordinated planning from a Financial Gravity Family Office Director who helps reduce surprises and build control.

Liquidity Without Liquidation: A Family Office Approach to Concentrated Wealth

Liquidity doesn’t require liquidation. A Financial Gravity Family Office Director helps you access capital, manage taxes, and preserve long-term wealth control.

From Compliance to Architecture: Elevating Tax Conversations with Affluent Clients

Advisor’s Alpha turns coordination into real wealth. See how a Financial Gravity Family Office Director helps you reduce costs, taxes, and risk with clarity.

Wealth Is a Team Sport: Why Coordination Outperforms DIY

Wealth is a team sport. See how a Financial Gravity Family Office Director turns fragmented DIY decisions into coordinated, compounding results.