Warren Buffett’s Legacy Will Echo In Eternity

Discover how Financial Gravity’s multi-family office services help families build lasting wealth with the discipline, clarity, and long-term vision inspired by Warren Buffett’s legacy.

Retirement Income Security

Discover the top 5 threats to retirement income—and how Time Optimized Planning™ helps retirees adapt, protect wealth, and plan with confidence in uncertain times.

Retirement Deserves a Strategy, Not a Guess

Retirement is a major life event—not just a number. Financial Gravity helps you create a personalized, adaptive plan for lifetime income and lifestyle security.

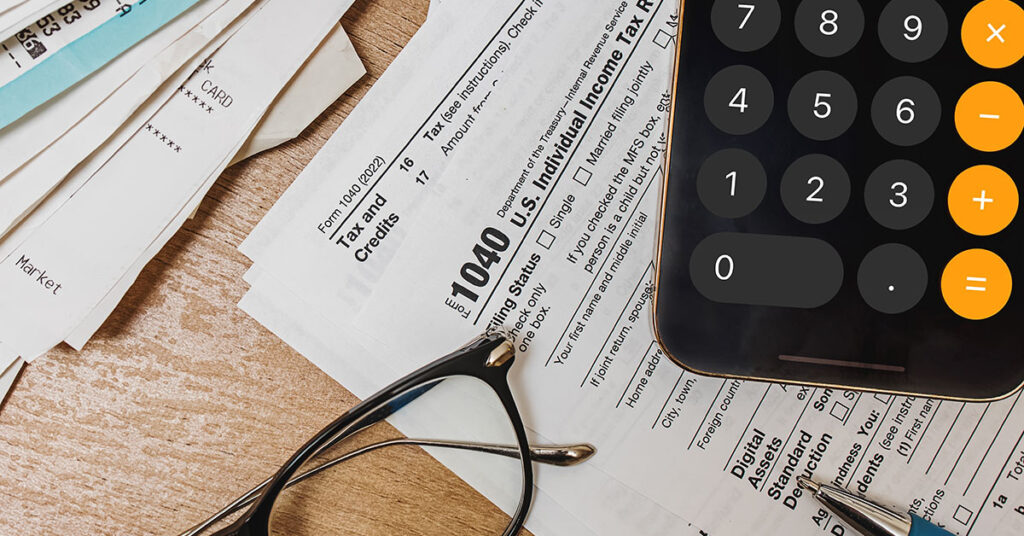

Come Back, Tax Season

Tax season is over—but the smartest planning starts now. Learn how Financial Gravity’s family office model creates lasting tax advantages and secures your legacy.

Defining Real Risk

Financial Gravity’s Real Risk Meter helps Family Office Directors define risk with precision—essential for guiding clients through volatile markets.

Fiscal Fitness

Learn how Financial Gravity Family Office Directors achieve tax-efficient financial wellness with strategies that protect, grow, and preserve wealth.

The Future of Taxes

Discover how AI, digital tools, and tax reforms in 2025 are revolutionizing tax filing, planning, and compliance for individuals and businesses.

The Weighing Machine

AI promises innovation, but at what cost? Explore 10 investment risks in AI, from market hype to high costs, regulation, and job disruption.

The Time Machine

Learn how Roth IRAs can be a powerful tool for tax-free wealth growth and legacy planning, inspired by Peter Thiel’s investment strategies.

How a Roth IRA Could Be the Greatest Investment Ever

Learn how Roth IRAs can be a powerful tool for tax-free wealth growth and legacy planning, inspired by Peter Thiel’s investment strategies.