Another tax season has ended, and this means you may have just had the most consequential financial conversation of your life. Or not, if that conversation didn’t look forward. If you didn’t at least begin to plan for the disposition of your low-cost-basis business or real property, or if you did not begin to outline what your legacy will be and how you might achieve it. How will you pass along your values along with your money? These are questions best answered using the combined expertise of tax, wealth, and risk management professionals working together.

Tax strategy can have a greater impact on your financial security than asset allocation, diversification, and risk tolerance. Those things are all important components of wealth management, but taxes can take half or more of your income and gains. The wealthiest families in America operate under a “taxes first” wealth management philosophy for this reason. They want to avoid estate taxes, of course, but they also want to convert, offset, or eliminate taxes wherever possible.

If you own a business that has appreciated greatly in value or real property with a low-cost basis, you could end up stroking the biggest check of your life when you liquidate. There are charitable strategies you can use to reduce your tax liability after a sale, but you have a great deal more flexibility by planning forward.

Waiting until after you sell doesn’t just affect you. Your wealth advisors lose a chance to provide input to your strategy. Tax pros who work collaboratively with asset managers tend to produce more thoughtful solutions. Fortunately, the democratization of the family office is making holistic planning a reality and is now helping mass affluent and affluent families enjoy the benefits the ultra-rich do.

It’s inconceivable to imagine a family office that does not have in-house tax strategy expertise, to include the legal structures and philanthropic tools that help a client reduce tax liabilities while supporting the client’s desires for their legacy. Ultra-high net worth families almost universally value tax advice as among the most important services of their advisors, but the affluent and even mass affluent cohorts also benefit from smart tax planning. In fact, the impact of saving on taxes may be greater on a person with $1,000,000 than one with $100,000,000.

You Should Learn About “Tax Alpha”

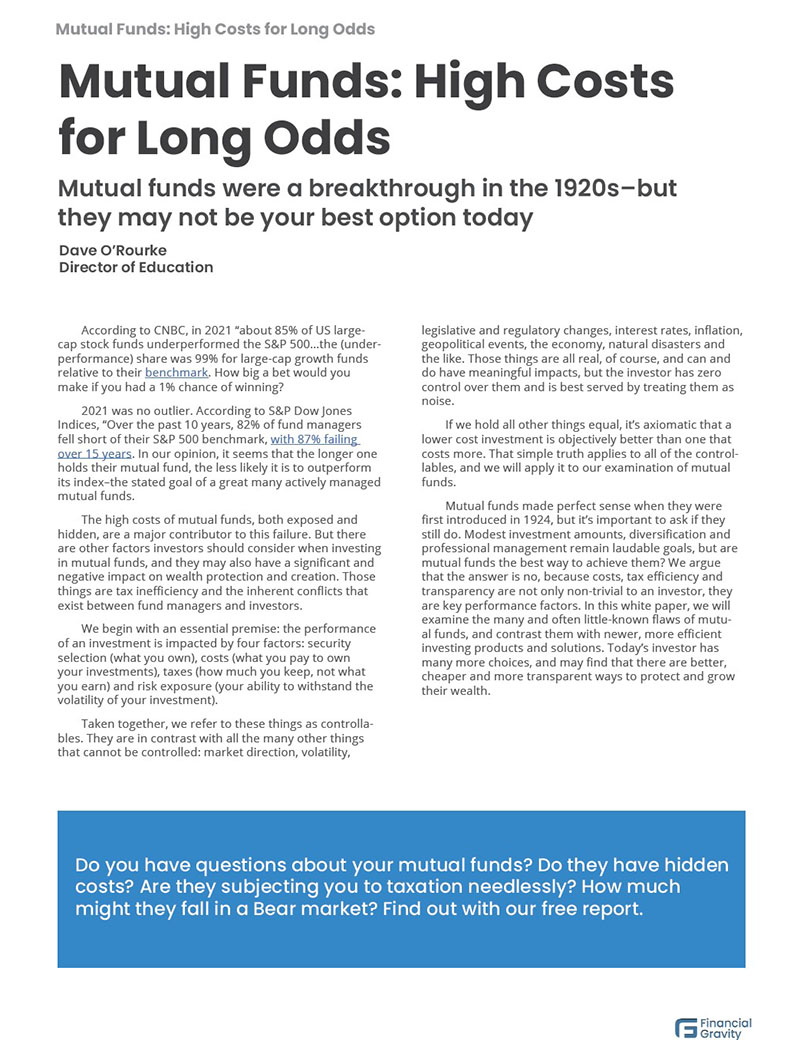

Mutual fund wholesalers, stock brokers, and even some advisors have tended to compete on portfolio performance for the past 100 years and more. Professionals who work with the ultra-rich and large institutional accounts know something different—that competing on returns will almost inevitably disappoint their clients.

Providing risk-adjusted returns that outperform their relevant benchmarks is very difficult to do. Ginsglobal reported in March of 2022 that “94% of U.S. Fund Managers underperform the S&P 500 over 20 years”. Their report went on to state, “Similarly, 92% and 93% could not beat the S&P Midcap 400 or the S&P Small Cap 600 respectively during this 20-year period (ending December 31, 2021).”

This pervasive failure isn’t cheap. Active managers tend to be notably more expensive than their passive ETF counterparts (who, by the way, do provide the return of their benchmark by definition). According to Investopedia, in 2022, the average index ETF ratio was 0.16%, while for an actively managed mutual fund, it was 0.66%. This is one of the reasons why family offices generally utilize passive strategies for their stock and bond allocations.

Instead of trying to outperform, family offices compete on “tax alpha.” Tax alpha is achieved through a combination of strategy, portfolio management techniques, and overlay applications. The offices are busy harvesting losses, managing capital gains, utilizing tax-advantaged accounts, and optimizing income and withdrawal strategies. The positive impact on compounding those results is known as alpha.

Even a modest amount of tax alpha can have a profound compounding effect over time, and that can mean greater financial security for the family and a larger legacy for their heirs. Tax alpha does another thing investors may appreciate: it justifies advisory fees, potentially turning an advisor into a profit center.

One of the most accessible strategies for advisors is tax-loss harvesting—intentionally selling underperforming securities, even if they are desired holdings—to offset capital gains and reduce tax liabilities. Thirty-one days after the sale, the position can be reestablished, but the loss has been realized. When you combine loss harvesting with disciplined rebalancing, you can boost compounding and keep your portfolio at the appropriate level of risk exposure.

Locating tax-efficient investments (like index funds or municipal bonds) in taxable accounts and tax-inefficient ones (like high-yield bonds or REITs) in tax-advantaged accounts can significantly boost after-tax returns. This practice is known as “asset location.”

Tax strategy can become even more crucial in your retirement years. By drawing income thoughtfully, annual tax burdens can be minimized, and needless, costly mistakes, such as creating Medicare surcharges or higher Social Security taxes, can be avoided. Other tax-smart strategies can include Roth conversions, required minimum distribution strategies, and charitable giving tools. All of these can create tax alpha.

Holistic Planning

Many families greet April 16th with a sigh of relief and simple gratitude that tax season is over for another year. For those who have not engaged in serious tax strategy, however, the next tax season should start today. Tax pros and wealth managers can do more for clients who have the time to plan ahead.

American families would be wise to consider the benefits of holistic planning that incorporates tax strategies into their financial planning and wealth management. This approach—the family office approach—stands in sharp contrast to product salesmanship and offers the additional benefit of greater transparency.

The wealth management industry is embracing the family office model because of its superior value proposition. Competing on portfolio performance is a game with the odds stacked against you, but focusing on tax alpha and then managing costs down and transparency up is something clients can actually benefit from.

Financial Gravity’s Turnkey Multi-Family Office Charter is a proven “taxes first” platform that provides access to next-generation technologies, deep subject matter expertise in planning, investment management, legacy planning, insurance and estate planning, and robust client service resources.